now loading...

For the global climate challenge, 2020 ended with great promise as both China and the United States joined the rest of the global community in setting a timeframe to reach net zero greenhouse gas emissions. 2021 has begun on a positive trajectory, as the shift to replacing fossil fuel electricity generation with renewable sources has continued with great speed and even seen the global oil majors actively participating in renewable energy auctions.

But while replacing high CO2-intensive electricity generation and combustion engines with cleaner alternatives will play a significant part in reducing greenhouse gas emissions, they alone will be insufficient to reach our 2050 net zero aims.

We need to start shifting our resources today to find solutions for those activities that will be difficult to electrify.

Hard to abate

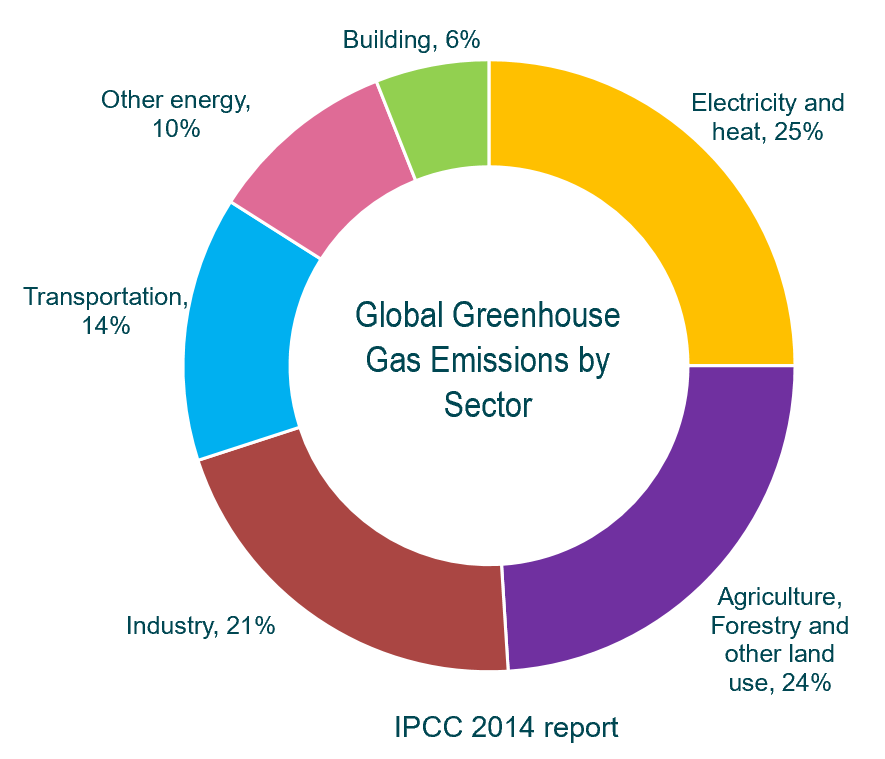

Within the transportation sector – heavy-duty vehicles, air travel and shipping account for 19% of global CO2 emissions and there is currently no feasible way to electrify these activities. Considering the cost and weight of the batteries, even with continuing technological advances, it’s unlikely electrification will be a solution by 2050 for these sectors.

In industry, the production of steel and cement accounts for 16% of global emissions and these areas also do not have viable paths to electrification.

In total, a whopping 35% of global emissions will require an alternative to electrification if we want to move away from oil and coal. The emerging alternative is hydrogen.

We have the technology today to produce hydrogen from carbon-free renewable energy sources, such as wind and solar power.

There are two key components to producing this emission free energy. First is the electrolyzer, which converts renewable energy into hydrogen. Then there is the fuel cell, where hydrogen is then converted back into a usable energy form, such as electricity. The largest impediment today is the cost.

Tellingly, we have seen offshore wind generation prices fall 89% over the last decade. As greater investments have been made, it is now the leading contender to replace fossil-fuel based power generation. There is every reason to assume that green hydrogen will follow a similar trajectory, especially now as it is being recognized as the best alternative to activities that cannot be electrified.

Green technology

President Xi Jinping’s adoption of the Paris climate goals is a welcome event – after all, when China commits to something it is not an idle commitment. It will be done with a huge amount of resources, effort and national will.

The former chief executive officer of a global company once commented that in order to make a return on investment, one needed to make the things China wants and avoid the things that China makes. Tellingly, China has decided to become a leader in solar and battery technology. The Chinese government has committed to supplying capital to companies which will make China the best in class and lowest cost operator in these areas. Outside of China it will be difficult for companies to invest in these areas and make an adequate return on investment.

In managing the M&G Climate Solutions fund, we have tried to stay away from areas where China has taken the lead and instead focused on those areas where investment in emerging climate technology is still required and where companies hold valuable intellectual property.

By investing in the hydrogen supply chain, namely a world leading electrolyzer manufacturer and a fuel cell IP company ( whose investors and customers include Chinese companies ), we are able to tackle the dual challenge of investing in companies that provide long-term impactful solutions to climate change and those that can also provide a strong return going forward.

Randeep Somel is fund manager at M&G Investments.