now loading...

In a world grappling with geopolitical tensions, trade disruptions, and policy uncertainties, the euro credit market stands out as a beacon of resilience and potential for Asian investors seeking diversification and stable returns.

For Asian investors, who often face exposure to US-centric risks like tariffs and global growth slowdown, euro credit offers a compelling avenue to hedge against these pressures while locking in favourable income levels, says Gonzague Hachette, investment specialist, fixed income, at AXA Investment Managers.

The euro corporate bond market continues to deliver solid performance despite recent volatility, buoyed by attractive yields, resilient fundamentals, and sustained investor inflows, attracting over €83 billion ( US$96.46 billion ) in net inflows into European fixed income funds in the first quarter of 2025 alone.

“This reflects a cautious yet opportunistic mindset among global investors,” Hachette says. “Yields remain elevated, providing an ideal environment for those looking to secure long-term value. However, divergence across sectors and countries underscores the need for selective strategies.”

Sectors like luxury goods and autos are vulnerable to external demand shocks, while financials and utilities benefit from conservative capital management.

This landscape allows Asian investors to diversify away from Asia-Pacific volatilities, such as supply chain disruptions or currency fluctuations, by tapping into Europe's more stable macroeconomic backdrop.

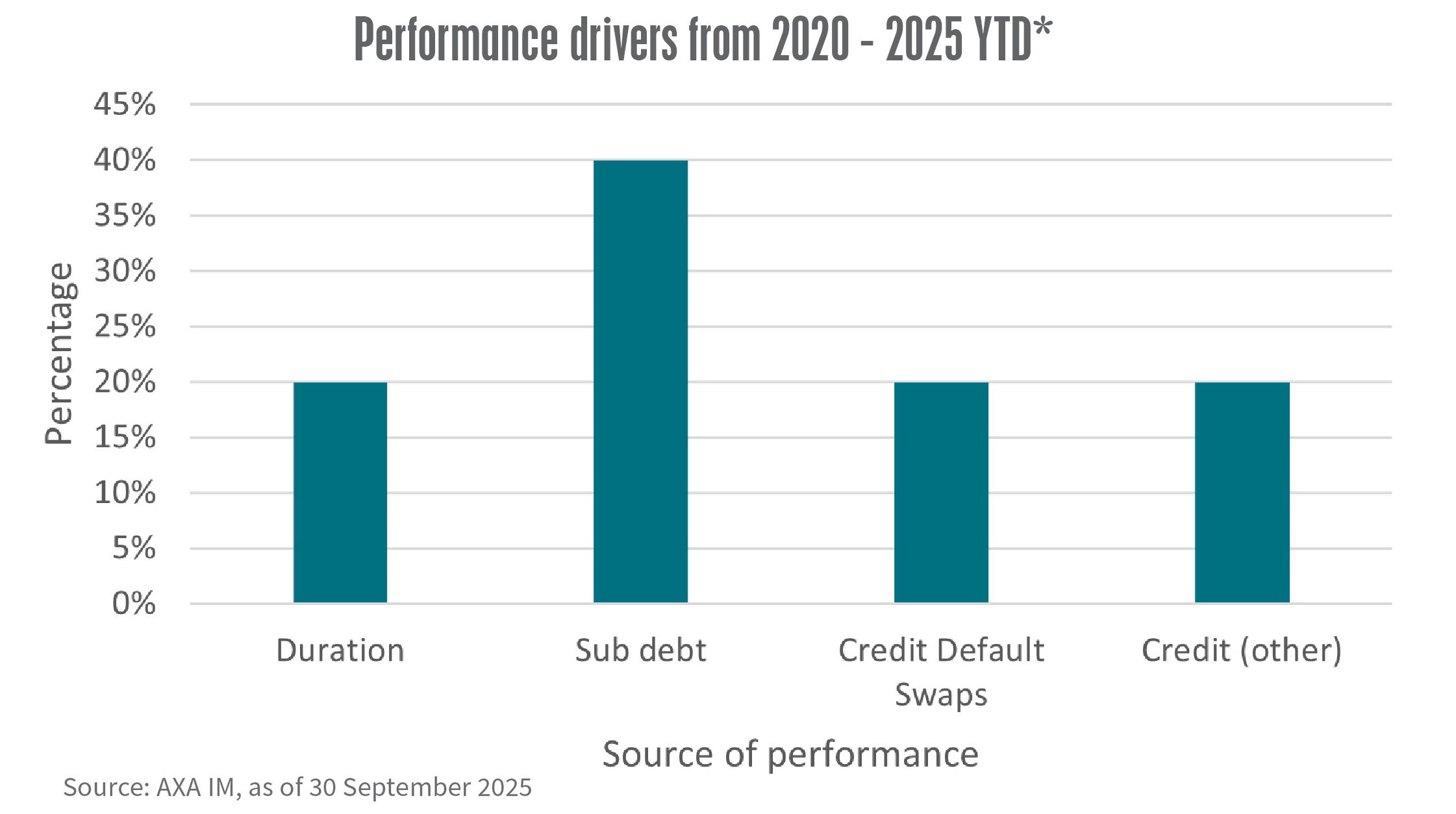

A key area of conviction is high beta credit, including subordinated debt and corporate hybrids, which have shown strong technical support and improving fundamentals.

High-yield spreads have tightened by over 150 basis points since April, with yields hovering around 5.1%. Selective positioning in this segment has significantly contributed to performance over the past five years. ( See chart )

For Asian portfolios, this high beta exposure can enhance risk-return profiles, offering higher carry amid credit tightening in some Asian markets.

Particularly promising is the banking sector, where eurozone fundamentals appear robust. European banks have seen equity prices surge over 55% year-to-date, underpinned by solid capital positions, resilient loan demand, and stabilizing net interest margins. From a fixed-income viewpoint, bank debt provides compelling value and diversification from US tariff impacts on global growth.

Credit fundamentals are sound, with low default risks and capitalization ratios exceeding regulatory thresholds. Investor appetite for subordinated bank debt is growing, as spreads remain attractive relative to other sectors.

Banks' focus on digital transformation and cost efficiency positions them to navigate structural shifts, delivering stable income to bondholders.

“Eurozone fundamentals look particularly supportive for the banking sector,” Hachette says, indicating that this insight resonates with Asian investors, who can leverage such strengths to mitigate risks from regional economic slowdowns or uncoordinated monetary policies.

Despite headwinds like rising political risks and potential tariff disruptions, Hachette advocates a flexible, active allocation approach. European issuers' strong credit quality enables them to withstand slowdowns, and persistent inflows into euro credit should cushion temporary dislocations.

For Asian investors, adopting this strategy – focusing on issuer selection with prudent financial management – can unlock attractive opportunities. By moving across sectors during volatility, portfolios can add value while maintaining resilience.

The euro credit market's blend of high yields, sectoral opportunities, and diversification benefits makes it an appealing choice for Asian investors in 2025.