now loading...

Investment in digital infrastructure continues to gain strong momentum, with funds flowing into data centres, cloud platforms, subsea cables, etc. Asia-Pacific lies at the epicentre of the global data centre expansion, driven by rapid advancements in artificial intelligence and cloud computing.

Global merger and acquisition ( M&A ) activity in the data centre sector reached a historical high of US$73 billion in 2024, according to Synergy Research Group. This surpassed the previous peak of US$52 billion in 2022, which was boosted by two mega deals, each valued at US$11 billion or more. In 2023, however, total value plummeted by 50% to US$26 billion.

Hyperscale data centres, built by cloud giants like AWS, Microsoft Azure, and Google Cloud, are massive, high-efficiency facilities designed to handle vast amounts of data processing, AI workloads, and global cloud services. Colocation data centres provide shared infrastructure where businesses lease space, power, and cooling systems, benefiting from cost savings, high security, and carrier-neutral connectivity. Edge data centres, on the other hand, are smaller, decentralized facilities positioned closer to end-users to support low-latency applications, including 5G networks, internet of things ( IoT ) devices, and real-time AI processing.

AirTrunk leads mega deals

Mega deals in the Asia-Pacific region led the surge in data centre M&As last year. In December 2024, for example, Blackstone and Canadian pension fund CPP Investments acquired Sydney-based AirTrunk for A$24 billion ( US$15 billion ), becoming the world’s largest-ever data centre deal.

Founded in 2016 with a focus on developing hyperscale data centres in Australia, AirTrunk opened its first facility in Sydney in 2017. Since then, it has expanded across the region, operating and developing campuses in Australia, Hong Kong, Japan, Malaysia, and Singapore.

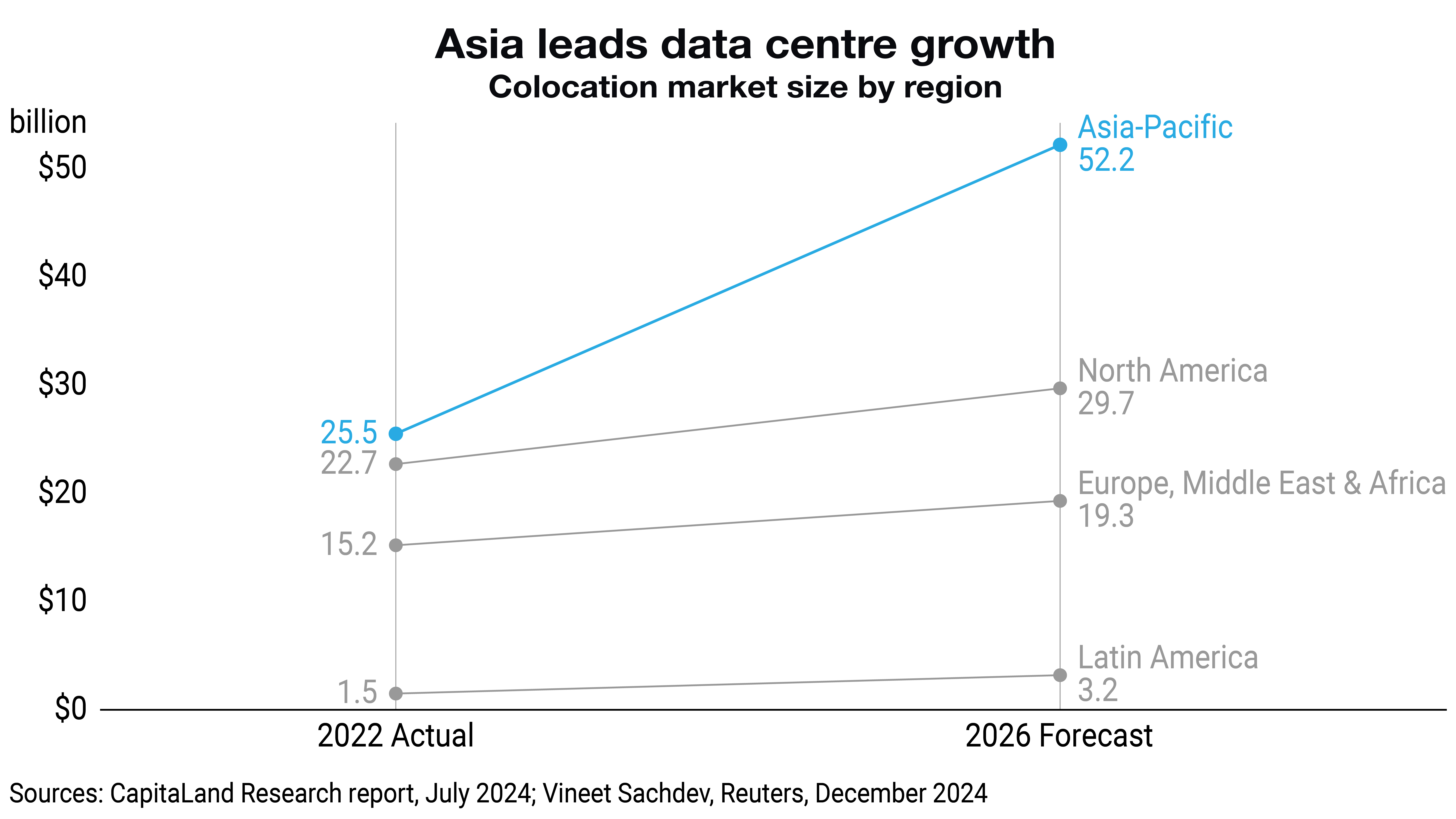

The APAC region is also emerging as a key colocation data centre market. The region is projected to expand from US$25.5 billion in 2022 to US$52.2 billion by 2026, or a compound annual growth rate ( CAGR ) of 20%, surpassing expansions in North America and EMEA, according to a CapitalLand Research report.

More players jump into fray

China has the highest number of data centres in Asia-Pacific, with 449 facilities as of October 2024, according to Statista. It is followed by Australia with 308 and Japan with 222.

Hong Kong and Singapore have long been key data centre hubs due to their strategic locations and robust infrastructure. However, the data centre building frenzy has spread to other Southeast Asian countries and India.

“We’re seeing hyperscalers not only leasing space in colocation data centres but also building their own dedicated facilities,” says Joshua Cole, partner, digital economy transactions, at global law firm Ashurst. “This trend is evident in Singapore, Malaysia, and now India, and it is expected to continue.”

India is also emerging as a key player, with 152 data centres as of October 2024, ranking fourth in the APAC region. “The cost of doing business, access to opportunities, and proximity to power sources have driven a significant surge in data centre development over the past 18 months,” Cole adds.

Moreover, India is becoming increasingly strategic in the global digital network. About a decade ago, a boom in transpacific networks connected the US West Coast to Asia. This was later followed by a major expansion of intra-Asian networks, driven by hyperscalers that push their infrastructure closer to key markets, according to Cole.

In February 2025, Meta announced plans to build a 50,000-kilometre subsea cable spanning the globe. The Project Waterworth initiative aims to connect the United States, India, South Africa, Brazil, and other regions, making it the world’s longest underwater cable project upon completion.

Singapore has traditionally been a major hub for data and delivery networks. Many international networks in the region converge in Singapore, but space constraints and high costs remain significant challenges. “Malaysia is increasingly attracting interest in the data centre industry,” says Cole. “Additionally, US-China tensions are driving both duplication and localization efforts in the sector.”

Malaysia offers incentives

Malaysia is actively pursuing efforts to gain a significant chunk of the data centre business. Johor, which is located near existing international networks in Singapore, benefits from Malaysia’s robust energy infrastructure, ensuring a reliable and affordable power supply for data centre operations. Additionally, the Malaysian state has significant potential for renewable energy sources, including solar, biogas, and biomass, supporting sustainable energy practices in data centres.

To further drive growth, the Malaysian government has introduced various incentives, including strategically designed tax breaks and a streamlined regulatory framework, creating a business-friendly environment conducive to data centre expansion in Johor.

AirTrunk opened its first data centre in Johor Bahru, the 150-megawatt AirTrunk JHB1, in July 2024, about a month before the announcement of its M&A deal.

More recently, in January 2025, Digital Edge, a leading developer and operator of interconnection and hyperscale edge data centres across Asia, and a portfolio company of Stonepeak, raised over US$1.6 billion in equity and debt to expand its data centre portfolio across Asia, including Malaysia.

Digital infrastructure M&A differs from other asset acquisitions due to its strict regulatory requirements, political sensitivity, and long-term nature. These assets – including data centres, fiber networks, and subsea cables – often require licensed ownership and national security approvals, particularly for foreign investors.